The Top 5 Risks To The Reign Of ‘King Coal’

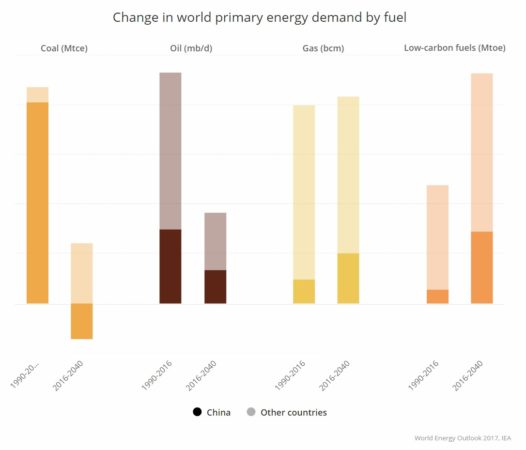

Among all the steps being taken to slow down global warming, and combat environmental damage, perhaps the most depressing , and toughest challenge is to fight the dominance of ‘King Coal’. Not only does coal continue to power the global energy mix, it remains the most difficult fuel to dislodge from its perch, thanks to its widespread availability, ease of extraction, transportation and existing technologies to harness it for power. Thus, China projects Coal’s share in its energy mix at an impressive 40% in 2040, from two thirds today. Consider the fact that this takes into account growth in consumption, thus ensuring total coal consumption actually rises or steadies at levels of 2023, thanks to better technology. India too, has a similar tale, a period of continued increases right upto 2030, before growth plateaus off. The share of coal moving from over 70% today to almost 50% even in 2040. For many observers, this dependence on coal dooms other well meaning efforts to limit global warming. So will coal continue to rule? We believe, while secure right now, like any monarch, King Coal has some serious threats building up. Almost any of these, on its own, may not finish the reign, but even two of these, together, could cause topple the long reign of coal. So here goes.

1. Better and Cheaper Battery Storage: Battery storage costs are projected to come down, and going by the buzz around it, could come down faster than expected.

At one point considered a technology that was immature and expensive, battery storage is now considered the key to carbon energy transition, having seen spectacular gains in cost-competitiveness since last year, as EV adoption and other users have increased demand. A recent analysis by research company BNEF revealed that the benchmark levelised cost of electricity (LCOE), for lithium-ion batteries has fallen 35% to $187 per MWh since the first half of 2018. $100 per KWh is considered the point at which demand will soar, as this will

Looking back over this decade, there have been huge improvements in the cost competitiveness of low-carbon options, thanks to more tech innovation, economies of scale, intense competition thanks to more players and more manufacturing experience collectively. The LCOE per megawatt-hour for onshore wind, solar PV and offshore wind have fallen by 49%, 84%, and 56% respectively since 2010. That for lithium-ion battery storage has dropped by 76% since 2012, based on recent project costs and historical battery pack prices.

These cost improvements in lithium-ion batteries mean new opportunities to balance a renewables-powered grid. Remember, thermal plants biggest advantage is the base load generation they do, to maintain grid stability. Batteries co-located with solar or wind projects are starting to compete, in many markets and without subsidy, with coal- and gas-fired generation for the provision of ‘dispatchable power’ that can be delivered whenever the grid needs it, not just when the sun shines or the wind blows.

Related Post

A sustained drop could lead to an upheaval in not just grid and renewable powered economies, but also make rooftop solar use cases explode, as houses and other customers like industries and large farms with large enough areas have an option to go off grid. Feeding a further cycle of lower baseload demand on the grid.

2. Hydro Storage: Pumped Hydro Storage, possibly the oldest and most conventional form of storing electricity has a very distinct and critical role to play in the transition to low-carbon energy sources.

Pumped hydro already constitutes 97% of electricity storage worldwide because of its low cost. And with the proportion of wind and solar in the electrical grid extending considerably, additional long-distance high voltage transmission, demand management and local storage is required for stability.

A new report released by the Australian National University (ANU) has revealed, that there are about 530,000 potentially feasible pumped hydro energy storage sites worldwide, with a total storage potential of about 22 million GWh.

To put that number into perspective, 22 million GWh is the rough equivalent of about one hundred times greater than the required storage capacity to fully supplement a 100 percent global renewable electricity system. An approximate guide to storage requirements for 100% renewable electricity, based on analysis for Australia, is 1 GW of power per million people with 20 hours of storage, which amounts to 20 GWh per million people.

The technology has a few limiting factors like high costs of installment and the long timeline for project development. Not to mention the possible environmental impact. But when pitted against setting up a coal power plant, factors like reliability, environmental impact and rapidly decreasing costs of both storage and renewable energy, leave no doubt. Against this backdrop, the hidden cost of coal power is not hidden anymore.

3. Clean Air Laws: China’s clean air laws are already the only thing limiting the growth of coal there. If and when India follows, it could be a big blow.

Chinese coal demand declined in 2016, (following a three-year trend) despite an increase in coal-power generation. The main driver for this apparent contradiction was coal substitution in small industrial and residential boilers; higher efficiency in power, besides the rush among the steel and cement industries to meet the country’s stringent air laws.

Based on market assumptions, and an active initiative of controlling its air quality, more than 100 Mt of coal currently used in the residential and industrial sectors (others than steel and cement) are expected to be replaced by natural gas over the next decade. Combined with the saturation of heavy industry growth, coal demand is forecast to decline through 2022, despite growth in coal conversion and in coal-power generation.

In India, the other major consumer of coal, despite rapid growth in renewables deployment, coal use is expected to rise. With a growing fleet of coal power plants running at less than 60% of capacity and robust power demand growth, coal-fired generation is forecast to increase at nearly 4% per year through 2022 in the subcontinent. And with an over-dependence on coal to meet its exponentially increasing energy demands and predicted growth in imports, the share of coal will decrease in the country’s energy mix as renewables continue to grow, but coal will remain a mainstay beyond 2040. That looks highly unlikely, as the country grapples with the dubious distinction of having 15 of the 20 most polluted cities in the world. Pressure to follow China with tougher clean air laws will be resisted only so long, or till technology, be it battery storage, or nuclear or something else, makes it possible. Thus, India, which has always been forced to be guided by price, will maintain loyalty to coal only as long as it is price competitive. A situation already under threat increasingly, and guaranteed to change by 2022 on present trends.

4. Nuclear Energy: 2019 has started with a bang by nuclear industry standards, in terms of support for the nuclear energy option. From Bill Gates to the US Senate which just introduced the Nuclear energy Leadership Act last week, to others, nuclear suddenly has a receptive audience again. If action follows, it could make a serious dent to coal demand. These are people who believe in climate change, but doubt the ability of solar and wind to provide answers. That makes them difficult to resist, if climate change accelerates.

Nuclear Energy provides a proven case model for rapid decarbonisation with economic and energy growth. And a glowing example of that is France. France decarbonised its’ grids decades ago and now it emits less than a tenth of the world average of carbon dioxide per kilowatt-hour. This was achieved with nuclear power, in barely two decades.

With the political will and better technology, China could replace coal without sacrificing economic growth, reducing world carbon emissions by more than 10 percent. Already, firms like Russia’s Rosatom have a bulging order book setting up nuclear power plants in countries that simply have no other way to meet their power needs with fossil, or renewables. These include high population regions like Egypt, Bangladesh, etc. Nuclear, when compared unfavourably with other options, is beginning to look positively good, when seen from a pure data perspective. As an industry expert said, the rare and unfortunate nuclear accidents have been treated like a terror attack, precisely because they were unexpected. While coal and thermal power fatalities mount quietly in the background, much like road accidents that kill millions each year.

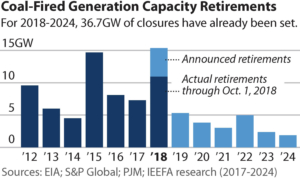

5. Drying Up of Coal Financing: The options for financing fresh coal mining and thermal plants continue to shrink. The only reason the coal industry still breathes easily is the fact that in its biggest markets, it remains essentially a government-backed and supported sector. That could change, not just with new governments, but also with more popular pressure. Be it the state-backed NTPC in India, or the top 5 thermal power generators worldwide, all China-based, these have needed a friendly government to make their life easier. Be it on issues of access to coal, pricing, or meeting pollution norms.

Over this decade, under relentless pressure from green activists as well as the emergence of viable alternatives, coal has been in retreat. In the US and Western Europe, it has been on a clear decline for some time now. Large sovereign wealth funds, besides Pension funds, endowments and international lenders like World Bank have pledged exits from financing coal power generation.

There are more than 100 globally significant financial institutions, with more than $10 trillion in assets under management—that have pulled out or restricted the access to the financing coal industry, says the IEEFA report “Over 100 Global Financial Institutions Are Exiting Coal, With More to Come”.

The report highlighted that, on average, there is one new announcement every two weeks. The World Bank announced the first-ever restrictions in 2013, with the 100th announcement in December 2018 coming from the European Bank of Reconstruction and Development (EBRD) removing three country exceptions to its coal finance ban. And, another 5 policies have been announced since the beginning of 2019 with moves coming from Nedbank of South Africa, Barclays Bank UK, Export Development Canada, and Varma of Finland.

“The pattern of tightening existing policies combined with new lending restrictions is creating a domino effect within the global financial industry while resulting in progressive strangulation of the thermal coal industry. Stranded assets are a clear financial risk for any institutions left funding the coal sector,” explains Tim Buckley, Director of Energy Finance Studies, IEEFA.

The unexpected $18 billion collapse into bankruptcy of Peabody Energy in 2016 and more recently the $150 billion drop in the market cap of General Electric shows the magnitude of capital destruction for investors who continue to ignore the energy system transformation.

However, globally, there’s still $420 billion in proposed coal plants in the pipeline, with construction finance in Southeast Asia, the last frontier for new coal expansion, coming largely from public institutions in South Korea, Japan, China, Southeast Asia and India.

Thus, King Coal, which ruled the 20th century and powered the biggest transformation in human history, is finally set to see a sunset on the empire, with survival into the second half of this century likely to be a vastly shrunken version of its existing size.